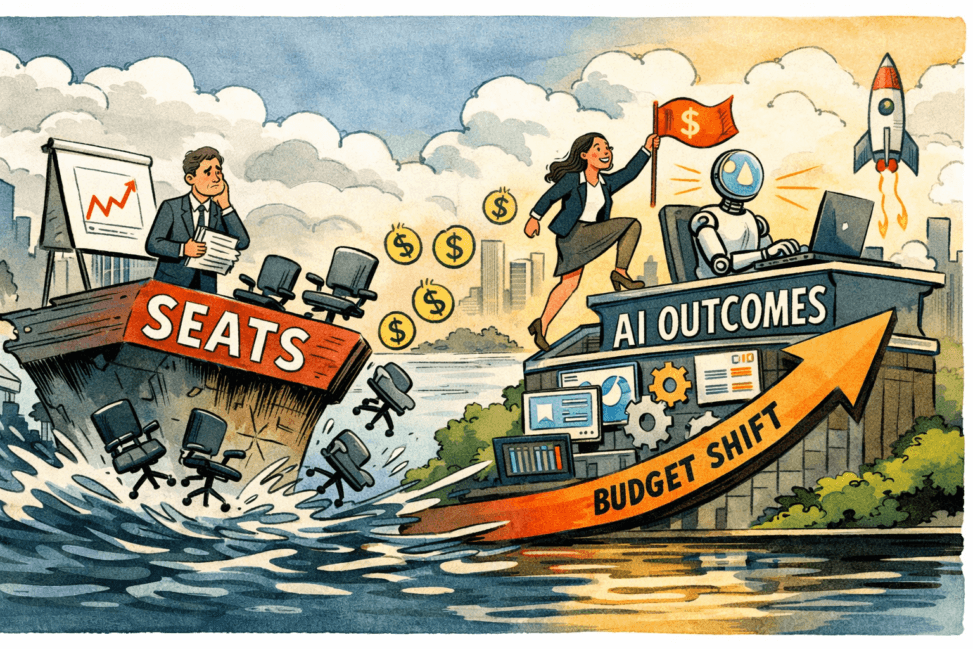

SaaS has always had its comfort blankets: seats, dashboards, admin consoles, and the sacred renewal motion. But something is changing! When AI can do the “clicky work”, summarise the backlog, raise the ticket, draft the runbook, and ship the workflow before your QBR deck finishes exporting, selling more logins isn’t a strategy anymore. Value is ! Budgets don’t vanish, they get reassigned and if you’re still charging for humans in a world optimising for fewer humans, you’re volunteering for contraction. If you can charge for outcomes in a world buying outcomes, you get to keep the margin and the multiple. (#JustSaying)

I do think that SaaS businesses that remain seat-count and UI-centric will see structurally weaker growth because budget is being reallocated to AI, while those that reposition into the AI budget can preserve multiples and growth.

So the relevant ROI question becomes: what return do you get from the set of moves that (a) protects existing revenue from seat and app-fatigue pressure and (b) captures incremental AI spend?

The macro backdrop (or why ROI is being repriced)

There are two external signals support the “budget reallocation” intuition even if you disagree with the exact magnitudes:

- Gartner forecasts worldwide AI spending of $2.52T in 2026 (+44% YoY).

- Gartner also forecasts worldwide IT spending of $6.15T in 2026 (+10.8% YoY). AI is therefore taking a growing share of the overall IT envelope.

If one line item grows far faster than the overall pot, something else gets squeezed. For a SaaS vendor, the investment thesis breaks into four return streams and three cost streams.

Return streams

- Revenue defended (avoiding seat compression)

If your pricing is materially seat-based, you are exposed to “same output, fewer humans” dynamics. Seat pressure is the quiet killer, where ROI here is not new ARR, it is ARR not lost (reduced downsell/contraction; steadier net retention).

- Revenue captured (entering the AI budget)

In the AI budget, not funding it, will be mainly through AI native experiences and outcome-based or consumption pricing. Here ROI is measured as AI attach, new modules, usage-based expansion, or monetised automation outcomes.

- Improved sales efficiency and time-to-value

An AI native workflow can reduce implementation friction and accelerate value realisation, which increases win rate and reduces payback for customers. With ROI manifesting as shorter sales cycles, improved conversion, and lower cost-to-serve.

- Strategic position (owning the data layer)

If you are the system of record, you remain essential because agents need a source of truth to read and write. Bottom line, ROI here often shows up in retention and platform stickiness, not immediately in growth.

Cost streams

A) Build costs (product + platform): AI native UX is more than adding a chatbot, needs to be workflow redesign and orchestration.

B) Run costs (inference + reliability): A useful yardstick is that inference averages ~23% of revenue for AI B2B companies (wide variance, but directionally important).

C) Trust and governance costs (security, safety, compliance): This is particularly true if you touch regulated workflows, your agentic layer carries assurance overhead that classic SaaS UIs did not.

Quick Decision Table

| Question | If Yes | ROI implication |

|---|---|---|

| Is >50% of revenue seat-based? | High seat compression exposure | ROI is mostly ARR defended (NRR protection) |

| Are you system of record (write authority)? | Agents must route through you | ROI includes platform rent and retention |

| Can you meter outcomes or consumption credibly? | You can price AI value | ROI includes AI attach expansion |

| Do AI features materially increase COGS? | Inference cost risk | ROI depends on pricing + usage controls |

| Is your UI/workflow “2019 vintage”? | Competitive gap | ROI includes win-rate uplift and churn reduction |

If you sell clicks, AI will always undercut you

So we know the ROI thesis is strongest where the commercial model is directly exposed to headcount. But, if you monetise human labour proxies such as seats and named users, the same outcome, fewer people dynamic hits you first. In that world, AI doesn’t have to replace your product to hurt you; it only has to reduce the number of people who need to touch it.

It’s also strongest when the product is mostly interface and thin workflow. UI-centric point solutions are vulnerable because agents and copilots can increasingly route around the interface, calling underlying systems and tools directly. If the value you sell is where the clicks happen, you’re competing with automation whose default setting is no clicks.

So, the safer ground is data gravity, where vendors that genuinely sit in the system-of-record layer can turn AI expectations into an upsell rather than a churn driver, because agents still need a trusted place to read and write, reconcile, audit, and hand off control. In that model, AI becomes a reason to pay more for the platform, not less.

Where this thesis becomes fragile, is when the economics are not engineered. If your AI feature-set drives heavy usage without pricing power, you create a margin trap: every incremental customer success is also incremental inference cost. You can grow adoption and still lose money, which is the worst kind of traction.

It is also fragile when you can’t evidence outcome pricing. Selling ‘we replace headcount’ requires instrumentation, baselines, and defensible attribution. Without that, outcomes becomes a story customers like in a pitch and unpick in procurement, and you end up discounting to close.

Finally, fragility also shows up when customers decide they want an AI layer over their apps. Some buyers will centralise AI in platform stacks and enterprise copilots, and vendors get squeezed into commodity tool roles underneath. In that world, you can build excellent features and still be bypassed, because the buyer is standardising the control plane elsewhere.